How Our Real Estate Investment Calculator Works

Zoom Playa Real Estate Calculator:

The Math Behind Every Number.

Zoom Playa Real Estate’s Calculator is built on transparent math. Every figure on this page comes from the same financial equations used by accountants and real estate analysts worldwide. The formulas, defaults, and worked examples below let you reproduce any number the calculator shows.

Table of Contents

- Introduction

- How to Use the Calculator

- Complete Formula Reference

- Mexican Real Estate Context

- Glossary

- Frequently Asked Questions

- Why is my Equity Buildup zero?

- Why does Cap Rate ignore my loan?

- What occupancy rate should I use?

- Why negative cash flow but still “good”?

- Why does exchange rate differ?

- Can foreigners buy property in Mexico?

- What if I want personal use?

- How do I email myself the PDF?

- Can I save my analysis?

- Methodology & Disclaimers

.

1. Introduction

What is This Real Estate Calculator?

The Zoom Playa Real Estate Investment Calculator is a comprehensive financial analysis tool designed specifically for evaluating vacation rental properties in Mexico’s Riviera Maya region, including Cancun, Playa del Carmen, Tulum, and Akumal.

Built by M H SABET for Zoom Playa Real Estate, this calculator solves a critical problem: comparing multiple pre-construction and existing properties side-by-side with accurate projections of cash flow, equity buildup, and total return over 5 years.

Who Built It and Why

Zoom Playa Real Estate created this tool to bring transparency to real estate investing in the Riviera Maya. Whether you’re comparing a $200,000 USD condo in Playa del Carmen with a $3,500,000 USD beachfront unit in Cancun, or analyzing how different payment structures (cash vs. financed vs. pre-sale) affect your returns, this calculator delivers precise, standardized metrics every investor needs. It is advised to contact one of Zoom Playa’s agents to get help using the calculator.

Ready to analyze your investment?

.

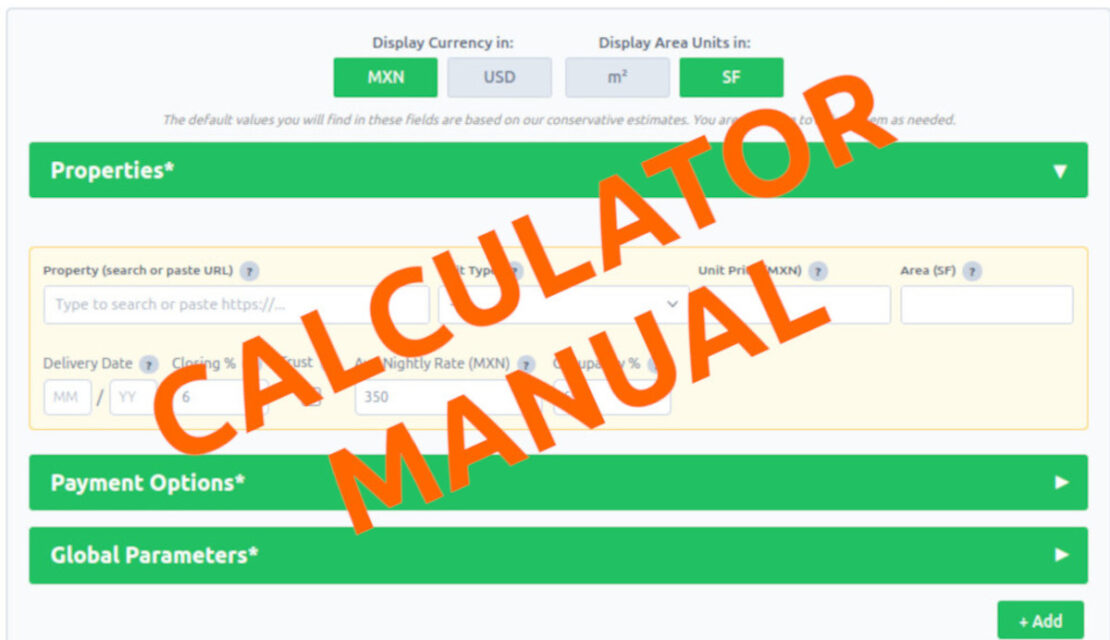

2. How to Use the Real Estate Investment Calculator

Display Currency & Area Units

At the top of the calculator, you’ll find two toggle switches:

- Display Currency: Toggle between MXN (Mexican Pesos) and USD (US Dollars). The calculator stores a per-property exchange rate snapshot when you add each property, preventing drift if rates change during your analysis session.

- Display Area Units: Toggle between m² (square meters) and SF (square feet). The conversion factor is 10.7639 SF per m².

Adding Properties

The Properties section (green accordions) is where you build your comparison list. The interface has a draft input row at the top where you enter:

- Property Search: Start typing a property name or URL. If the property is in our database, autocomplete suggestions appear with unit types and pricing. You can also add properties that are not in our database if you wish.

- Unit Type: Select the bedroom configuration (Studio, 1BR, 2BR, etc.). Some properties auto-fill pricing from our comparable data.

- Unit Price: The purchase price in your selected currency (MXN or USD).

- Area: Property size in your selected unit (m² or SF).

- Delivery Date (MM/YY): For pre-construction properties, enter the expected delivery month and year. You can find this date at the bottom of the description tab in all property pages. This is critical for cash flow projections because rental income doesn’t start until delivery + 3 months (promotional grace period).

- Closing Cost %: Typical Mexican closing costs (notary, registry, ISAI tax) range from 4-7% of purchase price. Default is 6%.

- Avg Nightly Rate: Expected nightly rental rate in your selected currency. This rate change from year to year and depends on the location.

- Occupancy %: Expected annual occupancy rate (0-100%). Realistic Riviera Maya ranges: Playa del Carmen 60-75%, Tulum 40-55%, Akumal 35-50% and Cancun 50-65%.

.

Payment Options

The second green accordion lets you choose how you’ll pay or finance each property. Select one:

Bank Loan

- Down Payment %: Percentage paid upfront (typical 20-30%).

- Interest Rate %: Annual percentage rate (APR).

- Loan Term (Years): Repayment period, commonly 15-25 years.

- Loan Start Date (MM/YY): When monthly payments begin.

Cash Purchase

100% of purchase price paid in cash upon immediate delivery. Enter the purchase date (MM/YY).

Pre-Sale

Developer financing for pre-construction properties. You define a custom payment schedule:

- Down Payment %: Initial deposit at signing (with date MM/YY). Developers usually ask a minimum of 30%

- During Construction %: Add none, one or more installment payments (each with % amount and date MM/YY).

- On Delivery %: Final payment when the property is delivered (uses the delivery date you entered in the Properties section).

The calculator displays these as %.

.

Global Parameters

The third green accordion contains financial assumptions that apply across all properties. These values are conservative defaults based on our market experience—you can adjust them:

| Parameter | Default (MXN) | Description |

|---|---|---|

| Internet | 600/month | Monthly internet cost |

| Water | 300/month | Monthly water utilities |

| Electric | 1,000/month | Monthly electricity depends on usage |

| HOA Rate | 40/m²/month | Homeowners Association fee per square meter. More amenities means higher costs per m2 |

| Property Taxes | 5,950/year | Annual predial (municipal property tax) depends on the size of your property |

| Property Mgmt Fee % | 20% | Percentage of rental income paid to manager. Usually between 20-30% |

| Mgmt Fixed Fee | 2,000/month | Fixed monthly management fee can vary from one property manager to the other |

| Exchange Rate Today (live rate) | 17 MXN/USD | Current MXN to USD conversion today |

| Exchange Rate in 5 Years | 19 MXN/USD | Projected rate for 5-year calculations based on the last 5 years |

| Capital Gain / Year | 7% | Annual property value appreciation depends on the location of the property |

| Yearly Inflation | 5% | Annual inflation affecting income and expenses (applied from Year 3 onward) |

Important: When you add a property, the calculator snapshots the current Global Parameters and attaches them to that property. Changes to Global Parameters after adding a property do NOT affect properties already added—each property is fully independent.

Click + Add to move the property from the draft row into your Selected Properties list.

3. Complete Formula Reference

Every formula below is the exact equation the calculator uses—not an estimate, not an approximation. Each one has been cross-checked against the calculator’s underlying logic and against industry-standard finance references.

However we know nothing is perfect. If you see a bug, wrong calculation or something that does not ultimately add up please report the issue to our admin team so we can fix it promptly. Best way to contact us about this is through whatsapp by clicking here.

3.1 Gross Rental Income

In plain English: How much money the property generates from nightly rentals before any expenses.

Annual Gross Rental Income = Nightly Rate × 365 days × Occupancy Rate

Monthly Gross Rental Income = Annual Gross Rental Income ÷ 12

Worked Example: 2BR Condo in Playa del Carmen

- Property Value: $200,000 USD

- Area: 85 m² (915 SF)

- Nightly Rate: $95 USD

- Occupancy Rate: 50% (0.50)

Calculation:

Annual = $95 × 365 × 0.50 = $17,337.50 USD Monthly = $17,337.50 ÷ 12 = $1,444.79 USD

Rental Income Timing: For pre-construction real estate with a delivery date, rental income doesn’t start immediately. The calculator applies a 3-month promotional grace period after delivery until the property has a few reviews and is listed on all relevant platforms. If delivery is in Jun 2026, rental income begins in Sep 2026. Properties without a delivery date generate income immediately.

.

3.2 Operating Expenses

In plain English: All costs required to operate the rental property, excluding mortgage payments.

HOA Fee + Property Tax (monthly) + Internet + Water + Electric +

Property Management (% of income) + Property Management (fixed fee) +

Fideicomiso Fee (if applicable)

Where:

HOA Fee = HOA Rate per m² × Property Area (m²)

Property Tax (monthly) = Annual Property Tax ÷ 12

Property Management (%) = Gross Rental Income × Management %

Property Management (fixed) = Fixed monthly fee

Fideicomiso Fee (monthly) = $500 USD annual fee ÷ 12 (if property requires fideicomiso)

Worked Example (Same 2BR Condo)

Given:

- Monthly Gross Income: $1,444.79 USD

- Area: 85 m²

- HOA Rate: 40 MXN/m²/month = $2.35 USD/m²/month (at 17 MXN/USD)

- Property Tax: 5,950 MXN/year = $350 USD/year (at 17 MXN/USD)

- Internet: 600 MXN = $35.29 USD

- Water: 300 MXN = $17.65 USD

- Electric: 1,000 MXN = $58.82 USD

- Management %: 20%

- Management Fixed: 2,000 MXN = $117.65 USD

- Fideicomiso: Foreign buyer, so YES → $500 USD/year = $41.67 USD/month

Calculation:

HOA Fee = $2.35/m² × 85 m² = $199.75 Property Tax (mo) = $350 ÷ 12 = $29.17 Internet = $35.29 Water = $17.65 Electric = $58.82 Management % = $1,444.79 × 0.20 = $288.96 Management Fixed = $117.65 Fideicomiso (mo) = $41.67 ───────────────────────────────────────── Total Monthly Exp = $788.96 USD

Critical distinction: Operating Expenses do NOT include mortgage payments. Debt service is calculated separately (see section 3.4).

3.3 Net Operating Income (NOI)

Corporate Finance Institute: NOI deep-dive →

In plain English: The property’s pure earning power before financing. This is what you’d keep if you owned it free and clear.

Monthly NOI = Gross Rental Income − Operating Expenses

Annual NOI = Monthly NOI × 12

Worked Example (Same 2BR Condo)

Monthly NOI = $1,444.79 − $788.96 = $655.83 USD Annual NOI = $655.83 × 12 = $7,869.96 USD

.

3.4 Monthly Real Estate Cash Flow (With Financing)

In plain English: The money left in your pocket each month after all expenses INCLUDING your mortgage payment.

For Cash Purchase or Pre-Sale:

Monthly Mortgage Payment = $0

Monthly Cash Flow = Monthly NOI

For Bank Loan:

Monthly Mortgage Payment = Calculated using amortization formula (see 3.5)

Worked Example (Bank Loan Scenario)

Given:

- Purchase Price: $200,000 USD

- Closing Costs: 6% = $12,000 USD

- Down Payment: 20% = $40,000 USD

- Financed Portion: $200,000 − $40,000 = $160,000 USD

- Closing Costs Financed: $12,000 USD (rolled into loan)

- Total Loan Amount: $160,000 + $12,000 = $172,000 USD

- Interest Rate: 6% annual

- Loan Term: 20 years

- Monthly Payment: $1,232.26 USD (see formula 3.5)

Monthly Cash Flow = $655.83 − $1,232.26 = −$576.43 USD This property has NEGATIVE cash flow in Year 1 — you pay $576/month out of pocket. However, you're building equity through principal paydown and appreciation. See ROI section for the full picture.

.

3.5 Loan Amortization (Monthly Payment Formula)

CFPB: how amortization works →

In plain English: How much you pay the bank each month to repay a loan with compound interest.

Where:

P = Loan Principal (financed portion + closing costs rolled in)

r = Monthly Interest Rate = Annual Rate ÷ 12

n = Total Number of Payments = Loan Term (years) × 12

Special Case: If r = 0 (interest-free loan):

Monthly Payment = P / n

Worked Example

Given:

- Loan Principal (P): $172,000 USD

- Annual Interest Rate: 6%

- Loan Term: 20 years

r = 0.06 ÷ 12 = 0.005

n = 20 × 12 = 240 payments

Monthly Payment = $172,000 × [0.005(1.005)^240] / [(1.005)^240 − 1]

= $172,000 × [0.005 × 3.31020] / [3.31020 − 1]

= $172,000 × 0.01655 / 2.31020

= $172,000 × 0.0071643

= $1,232.26 USD (rounded to $1,232 for downstream calculations)

.

3.6 Closing Costs

In plain English: One-time fees paid at the time of signing the deed to the notary to transfer ownership and register the deed of the property.

In pre-sale, this step usually comes around 3 to 6 months after delivery of the property depending on how fast the municipality emits the deed to the developer.

In resale or cash purchase through an escrow account the buyer usually pays the seller after signing the deed in the notary office.

Where:

Closing Cost % = 4-6% typical (covers ISAI, notary, public registry)

Fideicomiso One-Time = $1,500 USD (if foreign buyer in restricted zone)

For Bank Loan:

Closing Costs Financed = Purchase Price × Closing Cost %

Closing Costs Out-of-Pocket = $1,500 USD fideicomiso (if applicable)

For Cash Purchase:

Closing Costs Out-of-Pocket = (Purchase Price × Closing Cost %) + Fideicomiso

What is ISAI?

ISAI (Impuesto Sobre Adquisición de Inmuebles) is a Mexican state tax on real estate acquisitions, typically 2-4% of the cadastral value (which may differ from purchase price). Notary fees (~1-2%) and public registry fees (~0.5-1%) round out the closing cost package.

Worked Example (Bank Loan, Foreign Buyer)

Purchase Price = $200,000 USD

Closing Cost % = 6%

Closing Costs Base = $200,000 × 0.06 = $12,000 USD

Fideicomiso One-Time = $1,500 USD

─────────────────────────────────────────

Closing Cost Total = $13,500 USD

Distribution (Bank Loan):

Financed (rolled into loan): $12,000

Out-of-Pocket: $1,500 (fideicomiso only)

To get a more realistic calculation set your closing costs at 4% for properties above $650,000 USD and 7% for properties below $250,000 USD.

Although the tax section of the closing cost is always the same the notary service fees may differ from one notary to the next. So make sure to shop around and get a few quotes from different notary offices before making a decision and make sure to always close on your property with a notary that is in the same municipality.

.

3.7 Cap Rate (Capitalization Rate)

Investopedia: full background on cap rate →

In plain English: The return you’d get if you paid all cash. It measures the property’s earning power independent of financing.

Where:

Annual NOI = Net Operating Income for one full year

Property Value = Purchase Price

Worked Example

Annual NOI = $7,869.96 USD Property Value = $200,000 USD Cap Rate = ($7,869.96 / $200,000) × 100 = 3.93% The higher your cap rate the better.

A "healthy" cap rate threshold is above 6%.

Below that, the property relies more on appreciation than rental yield.

Riviera Maya vacation rentals typically show 6-8% cap rates and

strong appreciation (7-10% annually) make the region a great investment

for those who know.

.

3.8 Cash-on-Cash Return

Investopedia: cash-on-cash return explained →

In plain English: The annual cash return relative to the actual cash you invested (down payment + out-of-pocket closing costs).

Where:

Cash Invested = Down Payment + Closing Costs Out-of-Pocket

Annual Cash Flow Year 1 = (Monthly NOI − Monthly Mortgage Payment) × 12

Worked Example (Bank Loan)

Down Payment = $40,000 USD Closing Out-of-Pocket= $1,500 USD Cash Invested = $41,500 USD Monthly Cash Flow = $655.83 − $1,232.26 = −$576.43 USD Annual Cash Flow Y1 = −$576.43 × 12 = −$6,917.16 USD Year 1 CoC = (−$6,917.16 / $41,500) × 100 = −16.67% Negative cash-on-cash in Year 1 is common for financed properties. As rents increase with inflation (applied from Year 3+) and the mortgage stays fixed, cash flow improves. Plus, you're building equity.

Worked Example (Cash Purchase)

Purchase Price = $200,000 USD Closing Costs = $200,000 × 0.06 = $12,000 USD Fideicomiso One-Time = $1,500 USD Cash Invested = $200,000 + $12,000 + $1,500 = $213,500 USD Monthly Cash Flow = $655.83 (no mortgage) Annual Cash Flow Y1 = $655.83 × 12 = $7,869.96 USD Year 1 CoC = ($7,869.96 / $213,500) × 100 = 3.69% Cash purchase shows positive cash flow from day one but requires 5x more capital upfront. Opportunity cost matters.

.

3.9 Equity Buildup (Principal Pay down)

In plain English: The portion of your mortgage payment that reduces the loan balance and increases your ownership stake.

Each monthly payment is split between Interest and Principal.

Principal portion = Payment − Interest for that monthInterest for Month M = Remaining Balance × Monthly Interest Rate

Principal for Month M = Monthly Payment − Interest for Month M

Annual Equity Buildup = Sum of Principal paid in 12 months

For Cash Purchase or Pre-Sale:

Equity Buildup = $0 (no loan to pay down)

Worked Example (Bank Loan, Year 1)

Given: Loan $172,000 at 6%, 20 years → Monthly Payment $1,232.26

Month 1:

Remaining Balance = $172,000

Interest = $172,000 × 0.005 = $860.00

Principal = $1,232.26 − $860.00 = $372.26

New Balance = $172,000 − $372.26 = $171,627.74

Month 2:

Remaining Balance = $171,627.74

Interest = $171,627.74 × 0.005 = $858.14

Principal = $1,232.26 − $858.14 = $374.12

New Balance = $171,627.74 − $374.12 = $171,253.62

...continue for 12 months...

Year 1 Total Equity Buildup ≈ $4,592 USD

(Principal portion increases slightly each month as interest decreases)

Why is my Equity Buildup zero? If you selected Cash Purchase or Pre-Sale, you don’t have a bank loan, so there’s no monthly principal paydown. Your equity growth comes purely from appreciation, not from loan amortization.

.

3.10 Real Estate Property Appreciation

In plain English: The increase in real estate value over time, compounded annually.

Property Value After N Years = Purchase Price × (1 + Appreciation Rate)^N

Appreciation Gain in Year N = Property Value After N Years − Purchase Price

Worked Example (7% Annual Appreciation)

Purchase Price = $200,000 USD

Appreciation Rate = 7% per year

Year 1 Value = $200,000 × 1.07^1 = $214,000

Year 2 Value = $200,000 × 1.07^2 = $228,980

Year 3 Value = $200,000 × 1.07^3 = $245,009

Year 4 Value = $200,000 × 1.07^4 = $262,159

Year 5 Value = $200,000 × 1.07^5 = $280,510

Total Appreciation After 5 Years = $280,510 − $200,000 = $80,510 USD

.

3.11 Break-Even Period

In plain English: How many years until cumulative rental cash flow offsets your initial cash investment (down payment + out-of-pocket closing costs).

Cumulative Cash Flow = Cash Invested

Break-Even Period = Cash Invested / Average Annual Cash Flow

Note: This metric EXCLUDES appreciation. It only measures when

rental income covers your upfront investment.

Worked Example (Bank Loan)

Cash Invested = $41,500 USD Year 1 Cash Flow = −$6,913 (negative) Year 2 Cash Flow = −$6,913 Year 3 Cash Flow = −$4,200 (inflation boosts income) Year 4 Cash Flow = −$1,800 Year 5 Cash Flow = +$800 Cumulative after 5 years = −$19,026 Break-Even Period: Not within 5 years (from rental income alone). However, total return including appreciation + equity is +$87,457 by Year 5. This is why break-even from cash flow alone can be misleading.

.

3.12 Total Return & ROI (5-Year)

In plain English: The complete financial outcome combining cash flow, equity buildup, and appreciation.

Total 5-Year Equity Buildup = Sum of Annual Principal Paydown (Years 1-5) = $0 for Cash/Pre-Sale

Total 5-Year Appreciation = Property Value After 5 Years − Purchase Price

Total Return = Total Cash Flow + Total Equity Buildup + Total Appreciation

Total ROI % = (Total Return / Cash Invested) × 100

Worked Example (Bank Loan)

Cash Invested = $41,500 USD Total Cash Flow (5Y) = −$19,026 USD Total Equity Buildup = +$25,973 USD (principal paid over 5 years) Total Appreciation = +$80,510 USD Total Return = −$19,026 + $25,973 + $80,510 = $87,457 USD Total ROI = ($87,457 / $41,500) × 100 = 210.7% This means every dollar you invested in Year 0 became $3.11 by Year 5.

Want help interpreting your results?

3.13 Inflation Adjustment

Investopedia: inflation and real returns →

In plain English: How the calculator accounts for rising costs and rents over time.

Gross Rental Income = Previous Year Income × (1 + Inflation Rate)

Operating Expenses = Previous Year Expenses × (1 + Inflation Rate)

Years 1-2: No inflation applied (values stay at Year 1 baseline)

Years 3-5: Inflation compounds annually at the specified rate (default 5%)

Why wait until Year 3? Year 1 is typically a partial year (rental income only begins after the 3-month post-delivery grace period for new construction), and Year 2 is the first full year at baseline rates. From Year 3 onward, both rental income and expenses compound annually at the inflation rate, keeping NOI margins relatively stable.

.

4. Mexican Real Estate Context

Closing Costs in Mexico

Mexican real estate transactions involve several mandatory fees:

- ISAI (Impuesto Sobre Adquisición de Inmuebles): State acquisition tax, typically 2-4% of the cadastral value (assessed property value, often lower than purchase price). Varies by state—Quintana Roo (Riviera Maya) is ~2-3%.

- Notary Fees: ~1-2% of purchase price. The notary is a government-appointed attorney who verifies the transaction, handles title transfer, and registers the property.

- Public Registry Fees: ~0.5-1% to record the deed in the state property registry.

- Total Typical Range: 6-9% of purchase price, depending on property location and price point. The calculator defaults to 6%.

.

Fideicomiso (Bank Trust)

Here is an article we published explaining in depth what is the fideicomiso in Mexico.

Basically, foreign buyers cannot directly own property within 50 km of the coast or 100 km of an international border (the “restricted zone”). The Riviera Maya is entirely within this zone, so foreigners must use a fideicomiso—a bank trust where a Mexican bank holds legal title on your behalf.

Costs:

- Initial Setup: Usually $1,500 USD one-time fee (included in closing costs).

- Annual Renewal: Usually $500 USD/year paid to the bank on the anniversary of closing.

Important: The cost of the fideicomiso changes depending on the financial institution you use. You have full ownership rights—the bank is just a trustee. You can sell, rent, renovate, bequeath, or cancel the trust at any time. The fideicomiso is valid for 50 years and is renewable indefinitely.

.

Property Tax (Predial)

Mexican property taxes are remarkably low compared to the US, Canada or Europe. The predial is an annual municipal tax based on the property’s cadastral value, not market value.

Typical rates in Quintana Roo: 0.1-0.3% of cadastral value per year. A $200,000 USD condo might have a cadastral value of $120,000 USD, resulting in ~$120-360 USD annual tax. The calculator defaults to 5,950 MXN/year (~$350 USD at 17:1 exchange rate).

.

Bank Financing for Foreigners

Mexican banks DO lend to foreigners with residency permit in Mexico:

- Down Payment: Typically 20-50% (higher than the 10-20% common in the US).

- Interest Rates: 9-13% annual.

- Loan Terms: 5-15 years common; 20-year terms available from some banks.

- Currency: Loans are usually denominated in MXN.

- Requirements: Proof of income, Mexican credit report, valid visa or residency.

Here is a complete guide we published about available financing to foreigners in Mexico with and without residency permit.

.

Pre-Sale vs. Cash vs. Financed

Pre-Sale (Developer Financing)

For new construction projects, developers offer installment plans with 0% interest:

- Typical structure: minimum 30% down, 30-50% during construction, 30-40% at delivery.

- There are always discounts available for higher down payments. Sometimes 25% discount for 90% down early during the construction period.

- No bank involvement, no credit check.

- Prices are often 20-40% below post-delivery market value.

- Risk: Delivery delays do happen (3-12 months typical). The calculator accounts for this by pushing rental income start date by 3 months in addition to the 3 months promotional period.

Cash Purchase

Immediate delivery, immediate rental income potential. Best for:

- Buyers with liquid capital seeking immediate cash flow.

- Investors who want to avoid debt and maximize NOI.

- Flippers targeting quick appreciation in high-growth areas.

Bank Loan

Leverage other people’s money to control more property with less capital. Best for:

- Buyers who want to preserve liquidity for other investments.

- Investors targeting appreciation—if property appreciates 7%/year but you only put down 30%, your cash-on-cash return amplifies.

- Portfolio builders who want to own multiple properties with the same capital.

.

Exchange Rate Considerations

The calculator captures a per-property exchange rate snapshot when you add each property. This prevents drift during your analysis session if the live rate changes. When viewing results in USD, the displayed numbers use the SAME rate that was used in the property’s MXN calculations, ensuring perfect consistency.

For 5-year projections, you can set a separate “Exchange Rate in 5 Years” parameter. The calculator interpolates linearly between today’s rate and the future rate when converting appreciation gains.

Realistic Real Estate Occupancy Rates by Area in 2026

Location, location, location…

The closer you are to the beach and bars/restaurants the higher occupation rates you will have.

It’s that simple.

| Area | Typical Range | Notes |

|---|---|---|

| Playa del Carmen | 60-75% | High year-round demand, walkable beach town |

| Tulum | 40-55% | Strong December-April, softer May-November |

| Akumal | 35-50% | Quieter, family-oriented, lower turnover |

| Puerto Morelos | 45-60% | Growing destination, near Cancun airport |

| Cancun | 55-65% | World renowned |

.

Real Estate HOA Realities

HOA fees in the Riviera Maya are significantly higher than US/Canada averages due to:

- Climate: Constant heat, humidity, and salt air accelerate wear. Pools, gardens, and facades require frequent maintenance.

- Amenities: Luxury developments include beach clubs, concierge, 24/7 security, gym, spa, multiple pools. The more amenities and services your property has the higher the HOA cost per m2.

- Typical Range: 30-60 MXN/m²/month ($1.75-3.50 USD/m²/month at 17:1 rate). A 100 m² condo might pay $175-350 USD/month.

Remember that ultimately you as the owner and all the other owners in the building, through the condo association, will decide on the amenities you want in your building and as such the cost you are willing to pay.

Looking at a specific property? Let us review it with you.

5. Real Estate Investment Glossary

| Term | Definition |

|---|---|

| ADR (Average Daily Rate) | The average price charged per occupied night. In the calculator, this is “Avg Nightly Rate.” |

| Amortization | The process of paying off a loan through scheduled, equal payments over time. Each payment covers interest + principal. |

| Appreciation | The increase in property value over time, expressed as an annual percentage (e.g., 7% per year). |

| Break-Even Period | The number of years until cumulative rental cash flow equals your initial cash investment (down payment + closing costs). Excludes appreciation. |

| Cap Rate (Capitalization Rate) | Annual NOI divided by property value, expressed as a percentage. Measures property earning power independent of financing. Formula: (NOI / Property Value) × 100. |

| Cash-on-Cash Return | Annual cash flow divided by cash invested, expressed as a percentage. Formula: (Annual Cash Flow / Cash Invested) × 100. |

| DSCR (Debt Service Coverage Ratio) | A lender metric comparing NOI to annual debt payments. Not calculated by this tool, but important for qualifying for loans. Formula: NOI / Annual Debt Service. Banks typically require DSCR ≥ 1.25. |

| Equity Buildup | The cumulative principal paid down on a mortgage loan over time. Each monthly payment reduces the loan balance, increasing your ownership stake. |

| Fideicomiso | A Mexican bank trust required for foreign buyers purchasing property within 50 km of the coast or 100 km of an international border. Costs: $1,500 USD setup + $500 USD/year renewal. |

| GRM (Gross Rent Multiplier) | Property price divided by annual gross rental income. Formula: Price / Annual Gross Rent. Lower is better (faster payback). Not explicitly shown in the calculator but can be derived. |

| HOA (Homeowners Association) | Monthly fee covering common area maintenance, amenities, security, insurance. In Mexico, typically charged per m² of unit area. |

| Inflation | The rate at which costs and rents increase annually. The calculator applies inflation starting in Year 3 (default 5% per year). |

| Interest | The cost of borrowing money, expressed as an annual percentage rate (APR). Each mortgage payment includes interest + principal. |

| IRR (Internal Rate of Return) | The discount rate at which the net present value (NPV) of all cash flows equals zero. Not calculated by this tool—requires more complex time-value-of-money modeling. |

| ISAI | Impuesto Sobre Adquisición de Inmuebles—Mexican state acquisition tax, typically 2-4% of cadastral value. |

| LTV (Loan-to-Value) | Loan amount divided by property value. Formula: (Loan / Property Value) × 100. If you put 20% down, LTV = 80%. |

| NOI (Net Operating Income) | Gross rental income minus operating expenses (excludes mortgage payments). Formula: Gross Income − Operating Expenses. |

| Occupancy Rate | The percentage of nights per year the property is rented. 50% = rented half the year (183 nights). |

| Predial | Mexican municipal property tax, based on cadastral value (not market value). Typically 0.1-0.3% annually. |

| Pre-Sale | Buying a property before construction is complete, typically with developer-financed installment payments at 0% interest. |

| Principal | The portion of a mortgage payment that reduces the loan balance (vs. the interest portion, which is the lender’s profit). |

| Restricted Zone | Areas within 50 km of the coast or 100 km of an international border where foreigners cannot directly own property. Requires a fideicomiso. |

| ROI (Return on Investment) | Total return divided by cash invested, expressed as a percentage. Formula: (Total Return / Cash Invested) × 100. “Total Return” includes cash flow + equity buildup + appreciation. |

.

6. Frequently Asked Questions

Why is my Equity Buildup zero?

If you selected Cash Purchase or Pre-Sale, you don’t have a bank loan, so there’s no monthly mortgage payment and no principal paydown. Your equity growth comes purely from appreciation (property value increasing over time), not from loan amortization.

Why does Cap Rate ignore my loan?

Cap Rate measures the property’s pure earning power, independent of how you financed it. It’s calculated as Annual NOI divided by Property Value—no mortgage payments involved. This lets you compare properties apples-to-apples regardless of down payment size or interest rate. If you want a metric that includes financing, look at Cash-on-Cash Return instead.

What occupancy rate should I use?

We always like to look at this in a conservative way. Riviera Maya averages:

- Playa del Carmen: 50-65%

- Tulum: 40-55%

- Akumal: 35-50%

If you’re new to vacation rentals, start at the low end. You can always adjust upward as you gain experience with your property’s booking patterns.

Why are some properties showing negative cash flow but still marked as “good”?

Negative cash flow in Years 1-2 is common when financing a property (mortgage payment exceeds rental income). However, the calculator’s Total ROI combines three components:

- Cash Flow: Might be negative early on.

- Equity Buildup: You’re paying down the loan principal every month.

- Appreciation: Property value is growing (default 7% annually).

A property with -$500/month cash flow but $80,000 in appreciation over 5 years can still deliver 200%+ total ROI. The calculator’s “Best Property” recommendation weighs all three factors.

Why does the exchange rate sometimes differ across properties?

When you add a property, the calculator snapshots the current “Exchange Rate Today” from Global Parameters in the 3rd green drop down and attaches it to that property. This prevents drift during long analysis sessions. If you add Property A when the rate is 17 MXN/USD, then later change the Global Parameter to 18 MXN/USD and add Property B, the calculator will use 17 for Property A and 18 for Property B. Each property is fully independent.

Can foreigners actually buy Real Estate in Mexico?

Yes. Foreigners can buy real estate anywhere in Mexico. Within the “restricted zone” (50 km from coast, 100 km from borders)—which includes the entire Riviera Maya—you must use a fideicomiso (bank trust). The bank holds legal title on your behalf, but you retain full ownership rights: sell, rent, renovate, bequeath, or cancel the trust at any time. Costs: $1,500 USD setup + $500 USD/year renewal. The fideicomiso is valid for 50 years and renewable indefinitely.

What if I want to live in the property sometimes (personal use)?

The calculator assumes 100% vacation rental use. If you plan to use the property yourself, reduce the Occupancy Rate accordingly. Formula: Occupancy Rate to enter = Typical Rental Occupancy × (1 − Personal Use Months ÷ 12). Example: 2 months of personal use = factor of (1 − 2/12) = 0.83. If the area typically achieves 50% rental occupancy, enter 50% × 0.83 ≈ 41%.

How do I email myself the PDF report?

Click the “Email Report” button at the top or bottom of the calculator. A modal will open where you enter your name, country, phone number (10 digits, no country code, no spaces—format: 5551234567), and email. The calculator generates a PDF with all your properties, projections, and comparison matrix, then emails it to you within minutes. Don’t forget to check your spam folder and mark the email as “Not Spam” + “Important” to ensure you don’t miss future emails from us.

Can I save my analysis and come back to it later?

Yes. The calculator auto-saves your properties and Global Parameters to your browser’s local storage for 24 hours. When you return to the page, your data will still be there (unless you cleared your browser cache or used Incognito/Private mode). For permanent backup, use the “Email Report” feature to send yourself a PDF snapshot.

.

7. Methodology & Disclaimers

Projections, Not Predictions

This calculator produces financial projections based on the assumptions you provide. It does NOT predict the future. Real estate markets are influenced by factors this tool cannot account for:

- Economic shifts: Recessions, currency devaluations, inflation spikes.

- Regulatory changes: New taxes, zoning restrictions, short-term rental bans.

- Market volatility: Tourism downturns, natural disasters, global pandemics.

- Property-specific issues: Construction defects, HOA disputes, flooding, title problems.

Always cross-check these projections with a licensed CPA, real estate attorney, and your broker before making any purchase decision.

We always advise everyone to use this calculator with one of our real estate agents to get the intended full potential from it.

.

Assumption Defaults

The calculator’s default values are based on Zoom Playa Real Estate’s conservative experience in the Riviera Maya market and as of 2026:

- Appreciation (7% annually): Historical average for Playa del Carmen and Tulum from 2015-2025. Some years were higher (10-12%), some lower (3-5%). No guarantee this continues.

- Inflation (5% annually): Mexican historical average. Applied to both income and expenses starting Year 3, keeping NOI margins relatively stable. The last 12 months inflation was higher than normal and we can already see it stabilizing.

- Occupancy Rates: Based on actual property management data from our portfolio. Your mileage may vary based on property quality, pricing, and management effectiveness.

- Closing Costs (6%): Conservative estimate for Quintana Roo. Actual costs may vary depending on property price, notary office and municipality.

What the Calculator Does NOT Include

- Vacancy Risk: The calculator uses a static occupancy rate. In reality, occupancy fluctuates month-to-month and year-to-year.

- Major Repairs: Roof replacement, hurricane damage, A/C system failure—these are not modeled. Budget an extra 1-2% of property value annually for reserves.

- Income Taxes: The calculator shows pre-tax cash flow. Consult a CPA about Mexican rental income tax (non-residents pay ~25% on net income) and US/Canada foreign tax credits.

- Selling Costs: If you sell in Year 5, you’ll pay broker commissions (~6-7%), capital gains tax (varies by residency status), and possibly ISR (Mexican income tax on sale). Not modeled here. Your notary closing cost to sell the property will be minimal around 0.5-1%

- Currency Risk: If you earn MXN rents but need to repatriate to USD/CAD, exchange rate volatility matters. The calculator uses a fixed rate for simplicity.

- HOA Special Assessments: Occasionally, HOAs levy one-time fees for major projects (repaving, facade repair). Not predictable in advance.

Verification Process

Every formula in this manual has been verified against the calculator’s underlying logic. Spot-checks were performed against industry-standard finance references.

The methodology above is consistent with formulas published by Investopedia, the Corporate Finance Institute, and the U.S. Consumer Financial Protection Bureau.

All formulas align with standard financial mathematics as taught in real estate investment courses and used by property analysts worldwide.

Ready to analyze your Riviera Maya investment?

Have questions? Contact us for a personalized consultation.

Zoom Playa Real Estate

Riviera Maya, México

© 2026 Zoom Playa Real Estate.

Calculator Created by M. H. SABET.

All rights reserved.